Is the UK foodservice market showing signs of recovery?

Meaningful Vision tracked the overall traffic trends by segment.

Consumer traffic in Janaury was recorded as the lowest this year but a positive turn on May's year-on-year traffic could be a sign of recovery for the UK foodservice market, a report by Meaningful Vision revealed.

According to Meaningful Vision's Competitive Intelligence System, consumer traffic for the top 120 chains (including fast food outlets, coffee shops, casual dining, and pubs) declined by 1% in the first half of 2024 when compared with the same period last year.

At the outset of 2023 the market was trending positively as it recovered from the pandemic years, however, traffic began to decline in the latter part of 2023, a trend that has continued into 2024. January saw a nearly 5% drop, but by May year-on-year traffic had turned positive with a 1% increase, followed by a 1.2% rise in June.

The declining trend seen in the 2nd half of 2023 was almost exclusively attributable to the high inflation rate, up nearly 20% in June 2023 by comparison with 2022. Prices had actually risen earlier, in Q1 and 2 of 2023, but consumer traffic only began its decline a few months later as consumers adjusted their habits. Q1 2024 continued to see declines despite an additional day in February and an early Easter, both of which served to boost numbers when compared to 2022. However, the outlook became more optimistic from Q2 2024

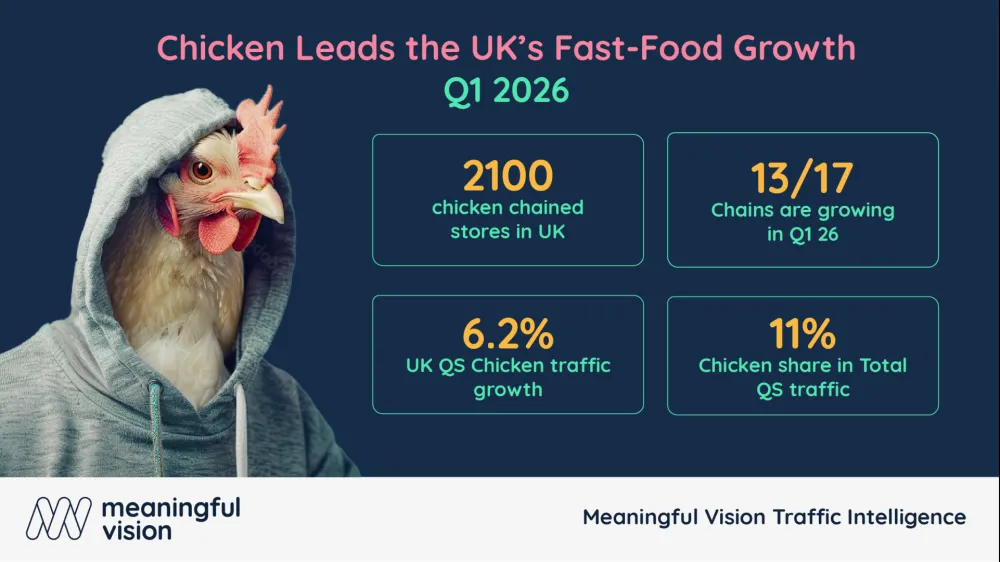

The fast-food segment, with a 0.7% decline, performed slightly better than restaurants with a 5.8% drop. Bakery and sandwich outlets were the only categories with positive traffic trends, showing a 4.4% increase over six months, followed by coffee shops with a modest 1.7% decline. Popular fast-food options such as fried chicken and burgers saw traffic decreases of 4.2% and 2.2% respectively, despite the rapid growth of American chains like Popeyes, Wendy’s and Wingstop entering the market for the first time.

Of importance to note is that most top chains are opening new stores, meaning same-store or like-for-like traffic is lower than numbers might otherwise suggest. Despite the top 120 chains increasing the number of their outlets by 3.2% in the first six months of 2024, like-for-like traffic declined by a concerning rate of 4%. The bakery and sandwich segment saw the highest rate of new openings, with chains like Gails, Pret, and Greggs contributing to a 5% growth rate, however, like-for-like traffic in bakeries remains negative as for all other segments.

Regional Differences

The fast-food industry in the UK exhibits significant regional differences, shaped by a variety of demographic and economic factors. London leads the way with a near 6% growth in fast-food traffic driven by a youthful population, a high concentration of job opportunities, and above average incomes. The city's diverse communities and a steady stream of international tourists also fuel a robust demand for a wide range of cuisines, ensuring a large and vibrant market.

In comparison, the top 10 largest cities outside London experienced more modest growth averaging at around 3%. The next 15 cities were largely unchanged, with traffic numbers remaining flat. By contrast, smaller cities faced a significant decline of 4.6% in fast-food traffic which negatively impacted the overall market numbers.

These regional disparities can largely be attributed to differing demographic and economic conditions. Smaller cities generally have lower population densities and fewer economic opportunities relative to their larger counterparts.

According to the Office for National Statistics (ONS), these areas also report rising unemployment rates, lower average incomes, and a higher proportion of families who may be opting for more economical home-cooked meals to offset increasing household expenses.

There are also noticeable differences within London itself. While Central London saw traffic growth, Greater London remained flat. This trend mirrors a broader pattern across the UK, where city centre locations are growing faster than suburban areas. In the first half of 2024, traffic in centrally located outlets increased by 3.6% on average, and by almost 8% in London, whereas the suburbs experienced a 2.3% decline. In all major cities, central locations saw traffic increases of 5-6%, partly driven by the fact that the majority of new fast-food outlets are concentrated in big cities and city centres.

An exception to these trends is the growth of bakery and sandwich outlets, which expanded not only in big cities and central locations but also in suburban areas across various regions.

Dayparts

Growth of morning traffic, a trend that started in 2023, continues into 2024. Traffic before 12 PM increased by 13.6%, raising its share from 24% to 27% of total daily traffic. Traffic from 12 PM to 3 PM also grew but at a slower pace of 4%, accounting for 31% of total daily traffic. Late day and dinner traffic declined by 12%.

Morning traffic growth was driven by the bakery and sandwich segment, as well the burger segment. The bakery/sandwich segment saw equal growth from 6-9 AM and 9-12 PM, while coffee shops also contributed positively, growing by 10% from 6-9 AM. Despite an overall lower volume of traffic during the 6-9 AM interval, this daypart witnessed twice as many additional customers in 2024 when compared with the 9-12 PM period. The burger segment showed the highest growth among the three described segments, with a 36% increase from 6-9 AM.

Chicken shops were the third-largest contributor to traffic growth from 12-3 PM. Coffee shops did not grow during this time but experienced most of their traffic decline from 3-6 PM.

CEO of Meaningful Vision Ltd. Maria Vanifatova said that whilst the overall foodservice market experienced a challenging first half of 2024, with a 1% decline in consumer traffic, there are encouraging signs of recovery.

"The resilience of certain segments, such as bakery and sandwich shops, combined with the positive impact of promotional activities and changing consumer behaviour, particularly around morning consumption, offer a glimmer of hope. Increased promotional activities, up 33% in Q2 2024 compared to Q2 2023, particularly by major fast-food brands focused on breakfast (e.g., McDonald's and Greggs) and lunch (e.g., KFC and Domino's), helped attract more customers. Pubs also benefited in June due to football’s European Cup, which traditionally draws large crowds. However, inflationary pressures, and a fiercely competitive marketplace exacerbated by new store openings, demand continued adaptation and a strategic focus on key consumer segments and dayparts by operators," Vanifatova said.