Who's drawing the most crowd in the UK's fast food scene?

Overall, fast-food traffic grew 0.8% in H1.

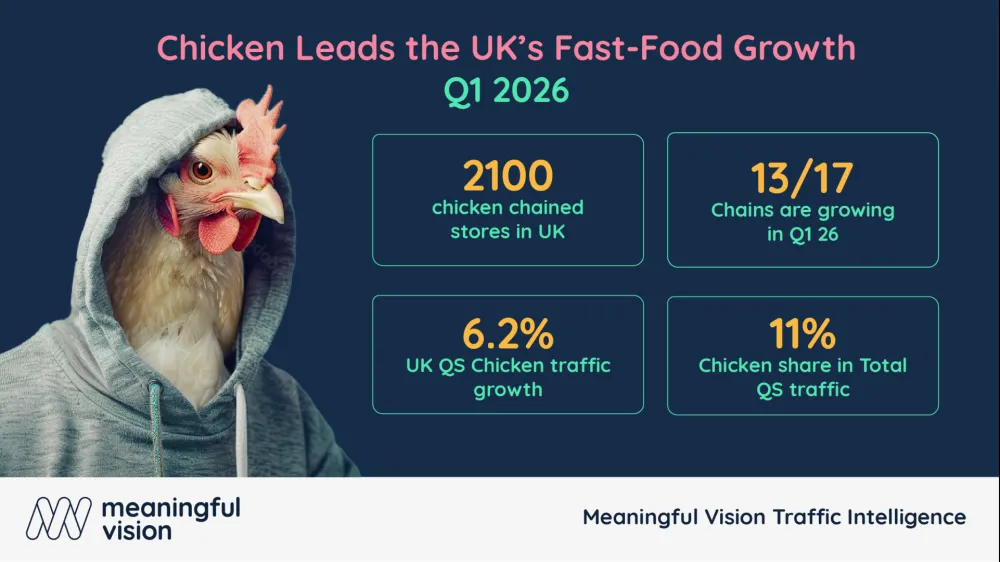

Chicken, coffee, and bakeries led footfall in the first half of the year, despite just 0.8% growth in overall fast-food traffic, a report by Meaningful Vision revealed.

Tracking over 60,000 UK outlets, the report revealed that quick-service chicken restaurants were the clear winners, with footfall up a strong 4.1% compared to the same period last year.

Meanwhile,coffee outlets also performed well, posting 3.9% growth of visits driven by consumer demand for affordable indulgences and convenience. Rounding out the growth categories, bakery and sandwich shops added 2.4%, reversing some of the declines seen in 2024.

Meanwhile, other segments faced significant pressure. Ethnic fast-food formats remained flat, whilst the burger category slipped into negative territory with a 3.1% decline in visits.

This downturn is largely driven by intensifying price competition and overlapping rivalry among fast-food players, all competing for the same pool of consumers.

The footfall dynamic also shifted throughout the first six months of the year. Whilst overall traffic was slightly stronger than in H1 2024, the second quarter showed a welcome lift with robust growth in April and May.

However, June brought the weakest year-on-year figures seen since early 2025, suggesting a slowdown in momentum. This trend is also reflected in the overall like-for-like guest numbers, which are still declining even in the fast-food sector, as traffic growth has been outpaced by new store openings.

"We are seeing a split in the market. The fast-food market is still largely driven by new openings. However, since guest numbers are not increasing on a like-for-like basis, simply expanding the number of outlets is a limited growth strategy in a market where demand is struggling,” Maria Vanifatova, CEO of Meaningful Vision, said

Vanifatova said it underscores the challenge for operators, with new restaurants drawing customers away from existing sites instead of generating fresh demand.

This highlights a key challenge for operators: new stores are often cannibalising traffic from existing locations rather than creating new demand.