A year in review of the UK’s fast food market

Chicken shops are winning whilst pizza delivery outlets showed slow growth.

The UK's fast-food market continues to evolve rapidly, with significant growth in new restaurant openings observed in the first nine months of 2024.

According to Meaningful Vision's latest data, compiled tracking various restaurant categories, including burger quick-service restaurants, chicken shops, bakeries and sandwich shops, coffee shops, Asian food, and pizza deliveries, amongst the 100 largest fast-food chains, the number of stores increased by 2.8% in comparison to the previous year. The largest number of new store openings was seen in Q2, with a 3.7% growth vs 2023.

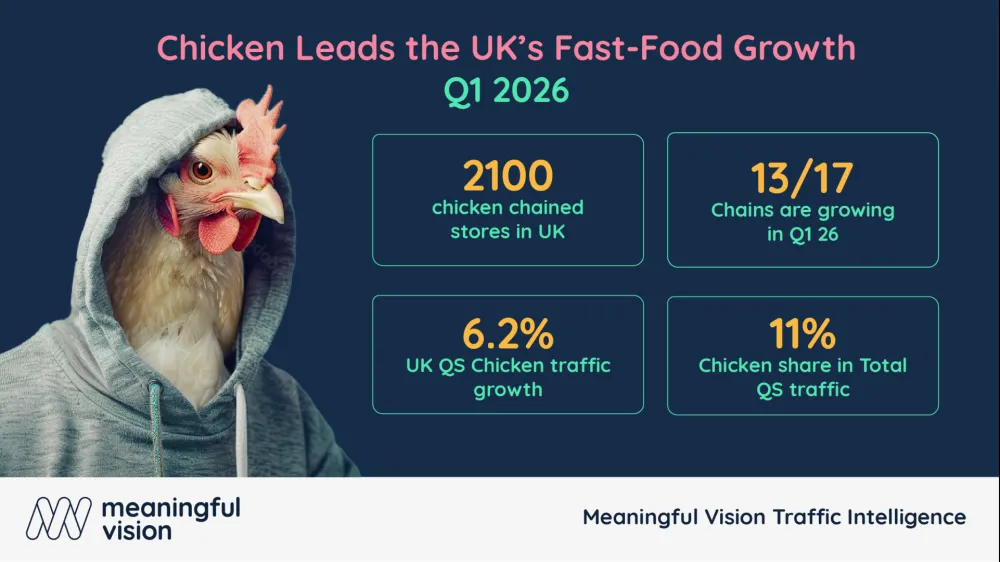

Chicken shops boom

Chicken has emerged as a major growth driver, with a remarkable 7% increase in the number of outlets. Both established chains like Morleys, Pepe’s, and new entrants from the US, like Popeyes and Wingstop, are contributing to this trend.

Ethnic fast food was #2 in terms of growth at almost 7%, mostly thanks to strong performances from Chopstix and German Doner Kebab.

Coffee shops experienced a 3.6% growth, fueled by chains like Costa Coffee, Starbucks, and Black Sheep Coffee.

Bakeries and sandwich shops saw a 2.6% increase, with Greggs, Gails, and Pret A Manger leading the charge.

Burger chains maintained steady growth, increasing by 2.5% due to McDonalds, Five Guys and Wendy’s.

Pizza delivery outlets experienced only 0.4% growth.

Regional dynamics

There were around 1200 chain restaurant openings in the UK between September 2023 and September 2024. The average rate of new outlet openings in the UK is 2.8%. Northern Ireland leads the way with a 9.5% growth rate, followed by England with a 3.1% increase. Scotland and Wales showed +2.5% and +2.8% respectively. Greater London opening rates were higher, but still below the national average of 2.6%, and London showed only 0.5% growth.

London, whilst demonstrating the slowest growth rate in percentage terms, was the biggest contributor to the overall number of new openings, accounting for 15% of all new stores.

Beyond London, the South East of England remains a significant and highly attractive market, with a substantial number of new openings occurring outside the capital.

Outlets density across formats

Meaningful Vision’s detailed analysis of regional outlet density highlights significant differences between various fast-food formats in UK cities and towns.

Burger restaurants are most evenly distributed across the UK, with an average of 3.5 per 100,000 people. However, cities like Portsmouth, Cardiff, Brighton, and Belfast stand out with higher-than-average concentrations.

Chicken outlets, with an average of 2.3 per 1000,000 people, are primarily concentrated in London and its large suburban areas like Watford, Croydon, Kingston-on-Thames, and Birmingham. In contrast, cities like Ipswich and Norwich, have significantly fewer options.

Glasgow, Portsmouth, and Cardiff boast the highest density of bakeries and sandwich shops.

Edinburgh, Chester, and London lead the way in terms of chain coffee shop density.

"The UK's fast-food market is experiencing significant growth, particularly in the chicken segment, with chains like Popeyes and Wingstop making notable inroads. While London remains a major market, contributing to a significant number of new openings, regions like Northern Ireland are demonstrating impressive growth rates. As competition is getting stronger, understanding these regional trends is essential for businesses to capitalise on the opportunities within this dynamic sector,” Maria Vanifatova, CEO of Meaningful Vision said.